When will mortgage rates fall?

(NerdWallet) – Mortgage rates are expected to go down sometime in 2024, but the decline probably won’t start in March. Instead, mortgage rates are likely to remain about the same because the economy hasn’t cooled off enough yet to cause them to fall.

When the economy grows robustly, and plenty of jobs are created, prices tend to go up. And when those three factors coexist, they combine to push interest rates higher. That’s what happened in February, and it’s unlikely that we’ll see a reversal of those trends in March.

A strong February leads into March

Rates went up in February, with the average rate on the 30-year mortgage at 6.78% in Freddie Mac’s weekly survey, up from 6.64% in January.

The culprit was a collection of strong economic data, released in February, that showed that the economy was running hot in late 2023 and into January. The overall economy grew at a 3.2% annual rate in the final three months of 2023. In January, the economy created a net 353,000 jobs and the core consumer price index accelerated. These signs of stronger-than-expected economic growth caused mortgage rates to rise in February.

Mortgage rates are unlikely to fall until there are unmistakable signs, for a few months in a row, that the economy is slowing down. We almost certainly won’t see those signs in March, despite two years’ toil by the Federal Reserve.

Eyes on the Fed

In an effort to slow the economy and get inflation under control, the Federal Reserve raised the overnight federal funds rate by 5.25 percentage points from March 2022 to July 2023. Inflation declined, as intended. The core CPI fell from 6.6% in September 2022 to 3.9% in January.

But inflation hasn’t fallen enough. The Fed’s goal is to reduce inflation to a 2% annual rate. The central bank will keep a floor under interest rates until inflation is unambiguously on the way to that 2% target. The Fed isn’t eager to cut the federal funds rate anytime soon.

This commitment was underscored by the title of a speech given Feb. 22 by Fed governor Christopher J. Waller: “What’s the Rush?”

Waller, who is a member of the Fed’s rate-setting Open Market Committee, said in his speech that the central bank must wait to verify that inflation is genuinely cooling off, “and this means there is no rush to begin cutting interest rates to normalize monetary policy.”

Usually Fed policymakers speak enigmatically, but sometimes they make themselves perfectly clear. That’s what Waller did with that speech. He sent an unmistakable signal that the Fed wouldn’t cut the federal funds rate at its March 20 meeting. With a rate cut off the table, there’s not much room for mortgage rates to fall in March.

Waller did say that he expects the Fed to cut short-term rates this year, but added, “the risk of waiting a little longer to ease policy is lower than the risk of acting too soon and possibly halting or reversing the progress we’ve made on inflation.” Therefore, there’s no rush.

Other mortgage rate forecasts

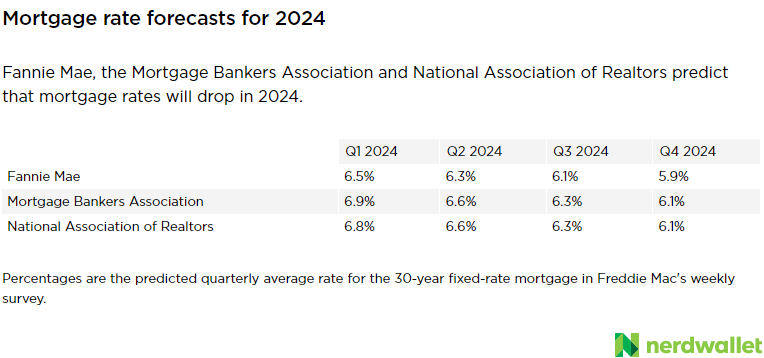

Fannie Mae, the Mortgage Bankers Association and National Association of Realtors predict that mortgage rates will gradually descend in 2024, to around 6% in the final three months of the year.

However, if the Fed keeps the federal funds rate unchanged through the first half of the year, don’t be surprised if forecasts are revised upward.

Looking back at February’s prediction

At the beginning of the month, I predicted that “mortgage rates might not change much in February.” Contrary to the prediction, mortgage rates did change in February: They started to rise in the first week and kept going up most of the month.

But the forecast served a purpose if it persuaded anyone to avoid waiting in vain for mortgage rates to fall in February.

I explained that rates “might remain relatively unchanged until markets believe the Fed is about to loosen monetary policy by cutting the federal funds rate.” That didn’t happen in February and it’s not going to happen in March.